Sometimes you just need to break loose and do something wild to feel like you’re really living. Maybe that means jumping out of a plane. Or maybe diving deep beneath the waves and exploring an underwater wreck.

Whatever your flavour of thrill, you don’t mind taking on some risk to feel a rush.

Chase your bliss, but just because you’re after a thrill you don’t need to be reckless about it! If you plan on participating in an extreme sport or activity, you need to know that you have the right protection in case something goes wrong.

Because right now, chances are you don’t.

You may assume that your regular life, auto, or travel insurance policies would cover you in the case of an accident no matter what you happen to be doing, but that could be a costly assumption. The vast majority of policies out there include specific provisions that exclude any sport or activity that are considered “high-risk,” “dangerous,” “hazardous,” or “extreme.” Just which sports and activities those terms include differ from insurance company to insurance company and policy to policy, but generally anything you might consider fast, high, or dangerous probably applies.

Let’s take a look at not only a few activities that will typically raise red flags for your insurance company, but also what you can do to make sure you can still qualify for affordable, effective insurance while chasing your thrill.

Skydiving

If jumping out of a plane thousands of feet in the air isn’t considered “extreme” I don’t know what is. Parachuting is a risky endeavour for experienced professionals let alone enthusiastic amateurs, so don’t be surprised if it is excluded from your current policies.

That doesn’t mean it’s impossible to insure yourself during a jump though. You can fortify your bargaining position with your insurance company by joining a skydiving organization. Ideally, seek out a professional club with its own dedicated drop zone. This will help control the risk factors associated with a jump making you a more insurable prospect.

If you want to make skydiving an ongoing part of your life, you can (and should) pursue solo dive certification, proving you are an experienced and accomplished skydiver. Only problem is, attaining that certification requires several tandem and supervised jumps as well as a large amount accrued free fall minutes, so it’s more of a long-term strategy to lower your premiums than something for a occasional or one-time jumper.

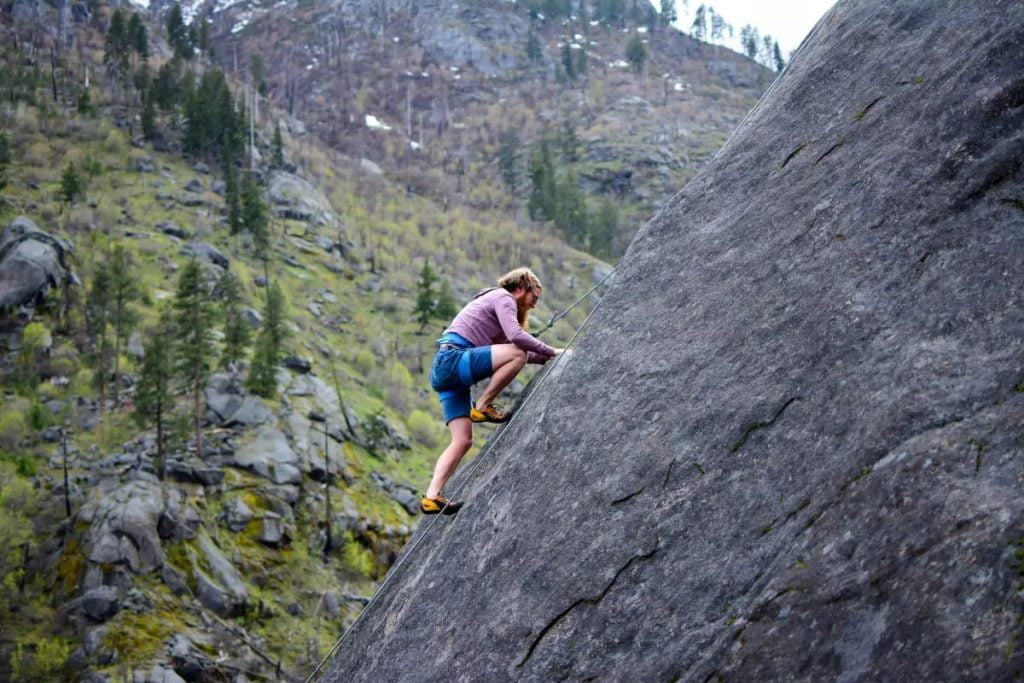

Free climbing

Mountain climbing of any sort is risky, but free climbing takes things a step further by upping the ante. A sport for those among us who are part mountain goat, free climbers takes to a cliffside with the intention of only using the bare minimum of climbing equipment to protect against falls. All upward progress is made using the climbers own hands, feet, and adrenaline, no assistance in the form of equipment or gear is allowed.

Free climbing means big bragging rights, but big bragging rights also means more danger. While safety equipment is still employed in a free climb, the strain of manually climbing every inch of a route, and the lack of hang-dogging or resting by suspended ropes means free climbers need to be in peak condition if they want to avoid a tumble. Add on the other risks common to any kind of climb such as rock-falls and poor wall conditions, and it’s no wonder underwriters shy away from free climbers.

Nothing is going to transform this into a “safe” sport, but you can minimize your risks to help your chances of securing favourable insurance. Letting your broker know what season you plan to climb in and which mountain and elevation can help. Making the climb as part of a group can be a huge asset as well.

MMA Training

MMA popularity has exploded across Ontario. Since being declared legal in 2010, gyms, dojos, and training centers have embraced the MMA lifestyle, taking in scores of enthusiasts and aspiring professional fighters. The record setting largest UFC event took place at Toronto’s Rogers Centre, and you can’t walk into a major department store without seeing MMA endorsed shirts, hats, and energy drinks. At this point, who doesn’t love MMA?

Well, probably your underwriter.

While it is easy to consider MMA like any other contact sport, insurance companies often have a less favourable take on it. The key difference is the intended consequence of the sport. While collisions and injuries are frequent in hockey and football, they’re incidental to the point of the game. When everyone follows the rules and wears the proper equipment, the level of injury among players should be fairly predictable and minor.

In an MMA ring, the whole idea is to harm the other guy until he can’t or won’t fight back. Fighters are supposed to incapacitate the opponent through striking or submission holds, both of which can result in serious injuries. Getting KO’d basically entails a minor concussion, while an arm-lock can turn into a broken arm very easily, especially when both fighters are still learning the ropes and don’t know how far is too far. While MMA is comparable to boxing, it also includes less safety equipment and more target-able areas (the entire body rather than just head and torso). While you may be willing to take your chances in the octagon, your insurance company might not.

As with similar sports, you will need to specifically address MMA training and participation in any personal or liability insurance policy. Even if you’ve already asked if your policy covers contact sports, ask specifically about MMA – you may find out it’s exempt. Belonging to an organized league or association with credible instructors and facilities can help reduce the premiums when you do find coverage.

Scuba diving

So, you’re going to strap on a heavy tank of compressed air and toss yourself off a boat into the freezing cold depths, what could go wrong? Plenty. Scuba diving is an inherently risky activity, no matter what precautions you take.

Scuba diving might not seem as extreme as it once did thanks to advances in technology and it’s popularity as a recreational activity, but from a safety perspective it still represents some astounding risks. There is always the chance of equipment malfunctions, diver disorientation, underwater obstacles, and water specific injuries like decompression sickness (a.k.a. “the bends”). Because of this, scuba diving tends to be another one of those activities that is subtly labeled “hazardous” and exempted from your policy.

That said, there are specific scuba diving policies available and ways to mitigate their cost. Going as part of a tour with provided equipment that is subject to inspection and accompanied by an experienced diving guide is a great way to reduce your risk. If you really want to go it alone, you’ll need to obtain proper diving certification before any insurance will even think about covering you.

There are other factors you should consider as well: the dive location and purpose can change things. Diving in a restricted space such as a cave or a wreck that limits mobility or requires a sidemounted tank configuration may require additional coverage. As can any kind technical diving (complicated dives that push the limits of human endurance and scuba technology). Just because you’ve cleared the occasional recreational underwater jaunt with your insurance, check again when you’re ready to step up to a more advanced (and dangerous) dive.

Know your Sport(s) and your Policies

There are few things out there that are completely un-insurable, but knowing how to navigate different policy options and advocate for your position isn’t always easy.

That’s why it’s crucial to talk with an experienced broker and let them know about any potentially risky vacation plans you have or dangerous new hobbies you might be developing. Your broker will help you find a policy that will protect you and your family should the worst occur, as well as help you strengthen your negotiating position to find the most favourable rate possible.

Jumping out of a plane is dangerous. Jumping out of a plane with no insurance is crazy.

Talk to your Staebler Insurance broker before making the leap!

0 Comments